Yes, in many cases, you can sell your house in Wisconsin even if you’re behind on payments or already in foreclosure. The key is timing: you usually still have options before the sheriff’s sale and often even up to the court’s confirmation of the sale (depending on your situation). Wisconsin Law Help

This guide explains:

- What “foreclosure in Wisconsin” really means (and where you are in the timeline)

- How long do you typically have

- Your best selling options (traditional sale, short sale, cash sale)

- What to do today if you’re trying to stop the foreclosure fast

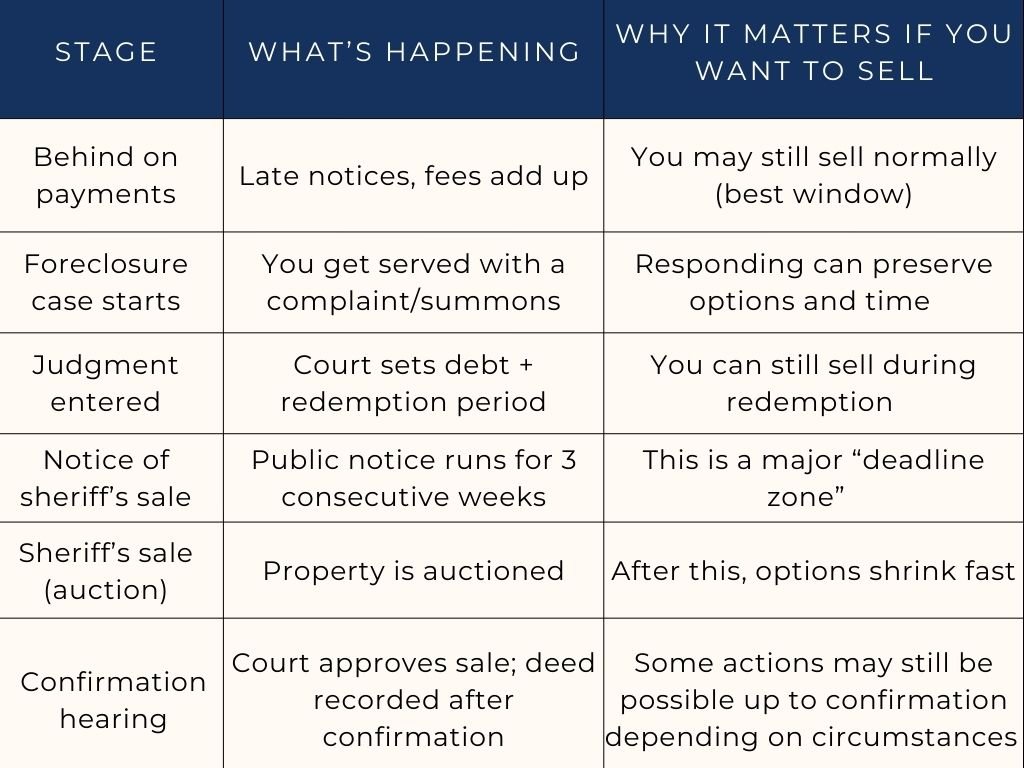

How foreclosure works in Wisconsin

Wisconsin uses a court foreclosure process (the lender files a lawsuit, and you receive a summons/complaint). If the lender wins (or you don’t respond), the court enters a foreclosure judgment. After that, Wisconsin law provides a redemption period before the property can be sold at a sheriff’s sale (auction).

Key terms you should know

- Foreclosure complaint: the lawsuit that starts the case.

- Judgment: the court order that sets the debt amount and starts the redemption clock.

- Redemption period: time between judgment and sheriff’s sale when you still own the home and can stop foreclosure by paying what’s required (often the full amount owed).

- Sheriff’s sale: the public auction after the redemption period ends.

- Confirmation hearing: a court hearing after the sale to approve it. You generally get notice if you appeared/responded in the case.

How long do you have to sell in Wisconsin?

There isn’t one single number, but most Wisconsin foreclosures take months, and many cases fall into a 6–18 month total timeframe from start to finish depending on schedules and redemption period length.

Wisconsin redemption periods (common scenarios)

For many homeowners, the redemption period depends on:

- When your mortgage was signed

- Whether the property is owner-occupied

- Whether the lender waives the right to seek a deficiency judgment (the amount still owed if the auction price is less than the loan balance)

According to Wisconsin legal-aid guidance:

- Mortgages signed before April 27, 2016: redemption is usually 6 months if deficiency is waived, or 12 months if not.

- Mortgages signed on/after April 27, 2016: redemption is usually 3 months if the deficiency is waived, or 6 months if not.

- If the home was listed with a real estate broker before judgment and you’re trying to sell in good faith, you may be able to request an extension (often 5 months instead of 3, or 8 months instead of 6).

The foreclosure timeline (what to expect)

Here’s a practical timeline you can use to understand where you are and what selling window you may still have:

3 ways to sell a house in foreclosure in Wisconsin

1) Traditional listing (best price, not always best timeline)

If you have time and your home is in sellable condition, listing can bring the highest offer. But foreclosure timelines can move faster than a traditional listing process.

When it makes sense:

- You’re early in the process

- The home can pass buyer inspections

- You can wait for financing timelines and appraisal

When it’s risky:

- You’re close to a sheriff’s sale date

- The property needs major repairs

- You can’t handle showings, cleaning, or buyer demands

If you list before the judgment (and you’re selling in good faith), you may be able to request a longer redemption period in certain situations, which can buy you time.

2) Short sale (sell for less than you owe – with lender approval)

A short sale is when the lender agrees to accept less than the total payoff. This can work, but it usually involves paperwork, waiting, and lender review.

Wisconsin foreclosure guidance notes that if the lender agrees, you may be able to sell for less than you owe during the redemption period (and you should understand the tax implications).

When it makes sense:

- You owe more than the home is worth

- You have time for a lender review

- You want to avoid the sheriff’s sale outcome

Main drawback: it’s not always fast – and “fast” is usually what you need in foreclosure.

3) Sell to a cash buyer (fastest way to stop the timeline)

If your priority is speed and certainty, selling to a legitimate cash home buyer can be the cleanest route – especially if the home is as-is and you don’t want repairs or delays.

This route is commonly used when homeowners need to:

- Stop foreclosure quickly

- Avoid showings, repairs, inspections

- Close on a deadline

At Prime Home Solutions, we buy houses as-is for cash across Wisconsin, including Milwaukee, Waukesha County, Racine, Washington County, Green Bay, and Appleton. If you’re facing foreclosure, the goal is simple: get a clear offer, confirm the payoff/steps, and close before your next deadline.

“I’m behind on payments” – does foreclosure mean I can’t sell?

Not at all.

Being behind on payments usually means one of two things:

- You’re not in a court case yet (you can usually sell normally), or

- You’re already in the court case (you may still sell during the redemption period before the sheriff’s sale).

In both situations, you want to move quickly because:

- Late fees and legal costs add up

- The process becomes harder (and more stressful) the closer you get to a sheriff’s sale date

What happens to the mortgage if I sell during foreclosure?

When you sell, the closing company typically requests a payoff statement from your lender and the mortgage gets paid from the sale proceeds.

- If the sale price covers the payoff + costs → the loan is satisfied at closing.

- If the sale price is less than the payoff → you’ll need lender approval (short sale) unless another arrangement exists.

Also, Wisconsin foreclosure guidance explains deficiency (the gap if the sale is less than what you owe) and notes that many lenders waive deficiency in order to get a shorter redemption period.

Warning signs you’re running out of time (don’t ignore these)

If any of these are true, treat it as urgent:

- You received a notice of sheriff’s sale (public notice runs for 3 weeks).

- You have a scheduled sheriff’s sale date

- You’re approaching a confirmation hearing date

-

You’re getting conflicting info from the lender/servicer

If you’re not sure what stage you’re in, check your case status with your county clerk of court and/or the documents you received.

The “Do This Today” checklist (practical + calm)

-

Find your next deadline

-

- Look for sheriff sale date, court dates, or the judgment date.

-

Know your goal

-

- Keep the home?

- Sell and walk away?

- Avoid a sheriff’s sale fast?

-

Get a payoff statement (or ask for one)

-

- You need this to know what number you’re trying to beat.

-

Pick the best sale route

-

- If time is tight: consider a cash offer route.

- If time is decent: consider listing or short sale.

-

Don’t wait for “perfect”

-

- In foreclosure, speed + certainty often matter more than squeezing every last dollar.

FAQs

Q: Can I sell my house in foreclosure in Wisconsin?

A: Yes, often you can – especially before the sheriff’s sale. Many homeowners can still sell during the redemption period after judgment and before the sheriff’s sale, but timing is critical.

Q: Can I sell my house if I’m behind on payments?

A: Yes. Being behind doesn’t automatically block a sale. The main issue is how far along the foreclosure timeline is and whether you can close before your next deadline.

Q: How long is the redemption period in Wisconsin?

A: It depends on your mortgage date and whether deficiency is waived. Many common scenarios are 3, 6, 8, or 12 months, with mortgages on/after April 27, 2016 often falling into 3 or 6 months.

Q: Do I get notice before a sheriff’s sale?

A: The sale is publicly advertised for three consecutive weeks before the sale date in the county where the property is located.

Q: What happens after the sheriff’s sale?

A: A court hearing is typically held to confirm (approve) the sale. If you participated in the case, you should generally receive notice of that hearing.

Contact Prime Home Solutions USA

If you’re managing a foreclosure and want a fast, stress-free sale, Prime Home Solutions USA can help. We buy homes as-is throughout Wisconsin – no repairs, no fees, no delays.

Call us today at (414)-800-9094 or fill out the form on our website to request your cash offer today!

Note: This is general information, not legal advice. Foreclosure rules and timelines can change, and each case is different.